![]()

100% Free L4M2 Files For passing the exam Quickly UPDATED Mar 19, 2026

L4M2 Dumps Questions Study Exam Guide

The Defining Business Needs certification exam covers a broad range of topics including the principles of business analysis, stakeholder management, requirements engineering, and business architecture. L4M2 exam is designed to test the candidate's understanding of these topics and their ability to apply them in real-world scenarios. L4M2 exam is conducted online and consists of 60 multiple choice questions that must be completed within 90 minutes.

NEW QUESTION # 54

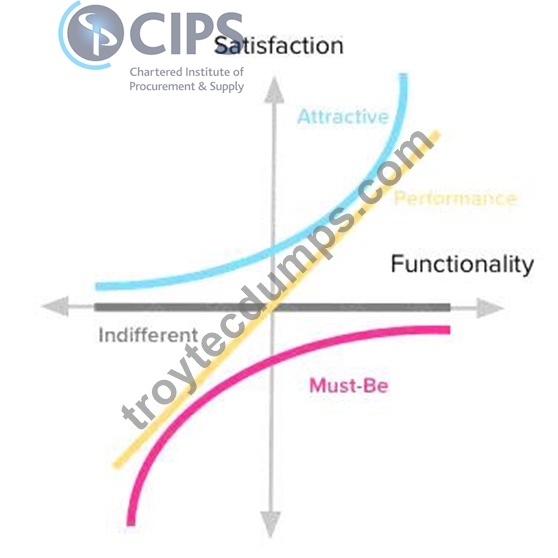

Daytona Ltd is developing a new product which is more environmental friendly. Though the objectives are set, the project team has no idea on which functions will be customers' favourites. Which of the following will help them decide the 'should-have' functions of the new product?

- A. Six Sigma

- B. Taguchi method

- C. Kano model

- D. Thomas-Kilmann model

Answer: C

Explanation:

The Kano model is useful in gaining a thorough understanding of a customer's needs. You can translate and transform the resulting verbatims using the voice of the customer table that, subse-quently, becomes an excellent input as the whatsin a quality function deployment (QFD) House of Quality.

The model involves two dimensions:

Achievement (the horizontal axis), which goes from the supplier didn't do it at all to the supplier did it very well.

Satisfaction (the vertical axis), which goes from total dissatisfaction with the product or service to total satisfaction with the product or service.

Dr. Noriaki Kano isolated and identified three levels of customer expectations: that is, what it takes to positively impact customer satisfaction. The figure below portrays the three levels of need: expected, normal, and exciting.

The Thomas-Kilmann Conflict Mode Instrument (TKI) is a conflict style inventory, which is a tool developed to measure an individual's response to conflict situations.

Genichi Taguchi, a Japanese engineer, proposed several approaches to experimental designs that are sometimes called "Taguchi Methods." These methods utilize two-, three-, and mixed-level fractional factorial designs. Large screening designs seem to be particularly favored by Taguchi adherents.

Six Sigma is a method that provides organizations tools to improve the capability of their business processes.

This increase in performance and decrease in process variation helps lead to defect re-duction and improvement in profits, employee morale, and quality of products or services.

Source:

- CIPS study guide page 171-172

- WHAT IS THE KANO MODEL?

LO 3, AC 3.4

NEW QUESTION # 55

Why should the buying organisation require the supplier to carry out acceptance testing?

- A. To compare between the account payables and account receivables

- B. To see whether the supplier engages in unethical business practice

- C. To get the approval from the senior management

- D. To check whether the product matches the specification

Answer: D

Explanation:

Acceptance testing, in the context of the engineering and software industries, is a functional trial performed on a product or prototype before it is put on the market or delivered, to decide whether the specifications or contract have been met. It also makes sure the quality and design of the product meet both contractual and regulatory obligations in terms of functionality, usability, durability, and safety.

If a product is found to be unacceptable at this stage, it can be sent back for modification, debug-ging, repair, or re-design before it can become a costly undertaking for the producer, as would be the case in a product recall.

NEW QUESTION # 56

This is the information on an organisation's activities over the past year

* Sale were $5,000,000. The value of accounts receivable was $450,000 at the start of the year and $525,000 at the end of the year

* The value of direct costs was $2,500,000 and 75% of this was bought on credit

* Indirect costs were $3,000,000 and 25% of this was bought on credit

* During the year the organization spent $1,500,000 on new assets and sold $150,000 of old assets. $1,000,000 of the spend on assets was funded by a bank loan

* The organization declared a dividend of $200,000 at the end of the year but this was not paid for another two months

* Opening balance was $175,000

Which of the following is the bank balance of that organization at the end of the year?

- A. $1,675,000

- B. $1,875,000

- C. $2,025,000

- D. $1,700,000

Answer: B

Explanation:

In this question, you should understand the concept of cash flow and formula of cash flow. Cash flow calculates the physical money moving in and out a company's bank balance. The cash flow from sale activity is:

cash flow from sale = account receivable at beginning of the year + revenue - account receivable at the end of the year = $450,000 + $5,000,000 - $525,000 = $4,925,000

75% of direct costs was bought by credit, therefore, the company spent 25% on direct cost: -$2,500,000*25/100 = -$625,000

25% of indirect costs was bought on credit. Cash flow out on indirect costs is: -$3,000,000*75/100 = -$2,250,000 Company spent $1,500,000 on new assets funded by a loan of $1,000,000. Cash flow out from this activity is -$500,000 Company received $150,000 from selling old assets Dividends have not been paid for another 2 months, thus, they are not accounted as cash flow out.

The bank balance at the end of the year is: $175,000 + $4,925,000 - $625,000 - $2,250,000 - $500,000 + $150,000 = $1,875,000 LO 1, AC 1.4

NEW QUESTION # 57

A procurement manager is discussing with other stakeholders about the scope and the implementation of the upcoming construction project. A stakeholder argues that the construction projects are often risky as the overall scope of the work can't be accurately estimated from the beginning. Furthermore, the project spans over a long period, the costs of materials can fluctuate widely. The procurement manager suggests that the pricing structure should be able to cover the supplier's costs plus 10% markup on total costs. This arrangement is known as...?

- A. Cost-plus award fee

- B. Cost-plus fixed-fee

- C. Cost-plus Fixed percentage

- D. Cost-plus incentive fee contracts

Answer: C

Explanation:

As you can see from the scenario, the procurement manager is suggesting to use cost plus pricing arrangement.

A cost-plus contract is an agreement to reimburse a company for expenses incurred plus a specific amount of profit, usually stated as a percentage of the contract's full price. These type of contracts are primarily used in construction where the buyer assumes some of the risk but also provides a degree of flexibility to the contractor.

Cost-plus contracts can be separated into four categories. They each allow for the reimbursement of costs as well as an additional amount for profit:

1. Cost-plus award fee contracts allow the contractor to be awarded a fee usually for good per-formance.

2. Cost-plus fixed-fee contracts cover both direct and indirect costs, in addition to a fixed fee.

3. Cost-plus incentive fee contracts happen when the contractor is given a fee if his or her perfor-mance meets or exceeds expectations.

4. Cost-plus percent-of-cost contracts allow the amount of reimbursement to rise if the contrac-tor's costs rise.

In the scenario, the procurement manager suggests a pricing structure that covers supplier's costs and adds 10% markup. This is cost-plus fixed-percentage.

Reference:

- Cost-Plus Contract Definition (investopedia.com)

- CIPS study guide page 30-36

LO 1, AC 1.2

NEW QUESTION # 58

The bargaining strength of suppliers is likely to be high in which of the following situations? (Select TWO)

- A. The buyer's spend is a high proportion of the supplier's revenue

- B. There is a limited number of suppliers in relation to buyers

- C. The buyer is large in size relative to the supplier

- D. The buyer's requirement is urgent

- E. The buyer is educated on supply markets

Answer: B,D

Explanation:

Comprehensive and Detailed Explanation (from CIPS L4M2: Supply Market Analysis) Supplier power is high when:

* Few suppliers exist relative to demand # less competition.

* Urgent demand gives suppliers leverage over buyers.

A and D would reduce supplier power; C (educated buyer) also weakens it.

Relevant CIPS L4M2 Sections:

* Porter's Five Forces - supplier power

* Market structure and urgency as power drivers

NEW QUESTION # 59

When analysing a market, the availability of substitute products or suppliers is the only competitive force to consider. Is this statement correct?

- A. Yes, substitute products and therefore cost is the source of all competition

- B. No, other forces include the threat of new entrants and bargaining strength of buyers and suppliers

- C. Yes, it is the only competitive force relevant to procurement

- D. No, availability of substitutes is not a competitive market force

Answer: B

Explanation:

Detailed Explanation:

While substitute products are an important factor, other forces such as new entrants, buyer and supplier bargaining power, and industry rivalry also significantly influence market dynamics. These forces are part of frameworks like Porter's Five Forces used in market analysis. Reference: CIPS Level 4, Market Environment Analysis.

NEW QUESTION # 60

Which of the following are the causes of material cost variance?

1. The buyer updates purchase-to-pay system to track payment and delivery

2. An unprocessed goods received note is missing

3. The employees must work overtime to catch up with the customers' orders

4. The purchase is made in emergency

- A. 2 and 4 only

- B. 1 and 3 only

- C. 1 and 4 only

- D. 2 and 3 only

Answer: A

Explanation:

The difference between the standard cost of direct materials specified for production and the actual cost of direct materials used in production is known as Direct Material Cost Variance. Material Cost Variance gives an idea of how much more or less cost has been incurred when compared with the standard cost. Thus, Variance Analysis is an important tool to keep a tab on the deviations from the standard set by a company.

Material Cost Variance can be due to less purchase price being paid than the standard or because of change in the quantity of material used. Thus, Material Cost Variance is made up of two components namely; Material Price Variance and Material Usage Variance.

Among the 4 options:

- 'The buyer updates purchase-to-pay system to track payment and delivery': The use of e-procurement system can increase the productivity and create labour cost variance, not material cost variance.

- 'An unprocessed goods received note is missing': If a goods received note is missing, the buyer won't pay for that batch, which create quantity variance.

- 'The employees must work overtime to catch up with the customers' orders': Overtime salary can cause labour variance, not material cost variance.

- 'The purchase is made in emergency': Normally, the price in emergency situation is higher than usual. This can cause price variance.

Reference:

- CIPS study guide page 57-59

- Material Variance | Cost, Price, Usage Variance Formula, Example - eFM (efinancemanage-ment.com) LO 1, AC 1.4

NEW QUESTION # 61

This is the information on an organisation's activities over the past year

* Sale were $5,000,000. The value of accounts receivable was $450,000 at the start of the year and $525,000 at the end of the year

* The value of direct costs was $2,500,000 and 75% of this was bought on credit

* Indirect costs were $3,000,000 and 25% of this was bought on credit

* During the year the organization spent $1,500,000 on new assets and sold $150,000 of old assets.

$1,000,000 of the spend on assets was funded by a bank loan

* The organization declared a dividend of $200,000 at the end of the year but this was not paid for another two months

* Opening balance was $175,000

Which of the following is the bank balance of that organization at the end of the year?

- A. $1,675,000

- B. $1,875,000

- C. $2,025,000

- D. $1,700,000

Answer: B

Explanation:

In this question, you should understand the concept of cash flow and formula of cash flow. Cash flow calculates the physical money moving in and out a company's bank balance. The cash flow from sale activity is:

cash flow from sale = account receivable at beginning of the year + revenue - account receivable at the end of the year = $450,000 + $5,000,000 - $525,000 = $4,925,000

75% of direct costs was bought by credit, therefore, the company spent 25% on direct cost: -$2,500,000*25

/100 = -$625,000

25% of indirect costs was bought on credit. Cash flow out on indirect costs is: -$3,000,000*75/100 =

-$2,250,000

Company spent $1,500,000 on new assets funded by a loan of $1,000,000. Cash flow out from this activity is

-$500,000

Company received $150,000 from selling old assets

Dividends have not been paid for another 2 months, thus, they are not accounted as cash flow out.

The bank balance at the end of the year is: $175,000 + $4,925,000 - $625,000 - $2,250,000 - $500,000 +

$150,000 = $1,875,000

LO 1, AC 1.4

NEW QUESTION # 62

Aircraft Category Manager, Harpal Patel, is purchasing several aircraft engines. He is seeking to determine which category of specification will be most appropriate. He decides on using a conformance-based specification. A conformance-based specification is most appropriate in which one of the following instances?

- A. When technology is changing rapidly in the market sector

- B. Where suppliers have greater relevant technical expertise than the buyer

- C. Where there are clear objective criteria for evaluating alternative solutions put forward by suppliers

- D. When technical dimensions are necessary for operational reasons

Answer: D

NEW QUESTION # 63

Which of the following are typically reasons why an organisation implements value analysis? Select TWO that apply:

- A. To shape and manage supply market

- B. To find cost reduction opportunities by optimising the components used

- C. To provide an outline business case for the specification

- D. To decide whether there will be sufficient surplus funds to reinvest in the business

- E. To determine the value of each component used

Answer: E

Explanation:

Value analysis is a systematic review of the production, purchasing and product design processes to reduce overall product costs. This can be accomplished through a variety of activities, including the following:

- Designing products to use lower-tolerance parts that are less expensive

- Switching to lower-cost components

- Standardizing parts across product platforms in order to achieve volume discounts

- Altering production processes to minimize the amount of production cycle time, thereby reducing labor costs

- Introducing automation to strip labor costs out of the production process

- Altering product packaging to lower its cost while still protecting the product The process is not a wholesale attack on costs. Costs are only reduced when the result will not im-pact the perceived level of quality experienced by customers, or the level of customer satisfaction.

NEW QUESTION # 64

Which of the following specific markets is most likely to have product shortage by nature?

- A. Services

- B. Agriculture

- C. Retail

- D. Financial

- E. Construction

Answer: B

Explanation:

Products used in agriculture can be subject to shortage due to natural disasters.

Reference:

LO 2, AC 2.1

NEW QUESTION # 65

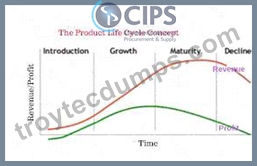

At which stage of product life cycle, price competition between sellers will be the most intense?

- A. Introductory stage

- B. Decline stage

- C. Maturity stage

- D. Growth stage

Answer: B

Explanation:

The term product life cycle refers to the length of time a product is introduced to consumers into the market until it's removed from the shelves. The life cycle of a product is broken into four stages-introduction, growth, maturity, and decline.

Chart, line chart Description automatically generated

Source: https://blueoceanoutsource.co.ke/the-product-life-cycle-concept/ At maturity stage, price competition sets in as more and more supply capacity has been added by new entrants, then the competition will be the most intense.

NEW QUESTION # 66

Lider Ltd is a leading bathroom furniture manufacturer in Indi

a. The company has more than 30 years experience in the market with extended knowledge of engineering and customers' taste. Lider is planning to launch a new type of bath fitting next year which offers Bluetooth connectivity and thermostat display. The company gathers a team of multi-disciplines, including engineering, procurement, sales and marketing. At the first team meeting, the project leader tells the team to discuss which functions will be valued by the customers, and how to deliver those functions with the lowest costs possible. Which of the following describes the process that the project team is undertaking?

- A. Cost analysis

- B. Just in time

- C. Value engineering

- D. Standardisation

Answer: C

Explanation:

From the scenario, you can see that the project team is developing a new product. They start with analysing the functions, and the costs of delivering those functions. This is a typical process of value engineering. You may read more on value engineering from the reference paper.

Reference:

- CIPS study guide page 171-173

- Value Analysis - Norwood Whittle (cimaglobal.com)

- A CASE STUDY ANALYSIS THROUGH THE IMPLEMENTATION OF VALUE ENGI-NEERING (researchgate.net) LO 3, AC 3.4

NEW QUESTION # 67

Rachel has issued a specification for spare parts out to global suppliers. Rachel has asked for these parts to carry a standard from the International Organisation for Standardisation. Is Rachel right to do this?

- A. No, as this standard will not be recognised outside of the UK

- B. Yes, as it is an appropriate and recognised standard

- C. Yes, as spare parts are the only things these standards apply to

- D. No, as these standards don't apply to spare parts

Answer: B

Explanation:

Detailed Explanation:ISO standards are internationally recognised benchmarks that ensure quality and safety, making them applicable across various industries, including spare parts procurement. This approach improves reliability and supplier compliance. Reference: CIPS Level 4, Standardisation in Procurement.

NEW QUESTION # 68

A company buys components from its supplier. However, the supplier has not sent the invoice to the buyer and the buyer will not pay until next month. How will that amount of money be shown in the financial statements of the buying organization?

- A. Accrued interest

- B. Accounts payable

- C. Accrued expense

- D. Tax liabilities

Answer: C

Explanation:

The buyer won't pay the supplier until next month. This is a liability to the buyer. This amount can be recorded as accrued expense or accounts payable. On the other hand, the supplier has not sent the invoice, so it should be accrued expense.

Both accounts payables and accrued expenses are liabilities. Accounts payable is the total amount of short-term obligations or debt a company has to pay to its creditors for goods or services bought on credit. With accounts payables, the vendor's or supplier's invoices have been received and recorded.

On the other hand, accrued expenses are the total liability that is payable for goods and services that have been consumed by the company or received. However, accrued expenses are those bills in which an invoice or bill has not yet been received. As a result, accrued expenses can sometimes be an estimated amount of what's owed, which is adjusted later to the exact amount, once the invoice has been received.

Conversely, accounts payable should represent the exact amount of the total owed from all of the invoices received.

Reference:

- CIPS study guide page 55-56

- Understanding Accrued Expenses vs. Accounts Payable (investopedia.com) LO 1, AC 1.4

NEW QUESTION # 69

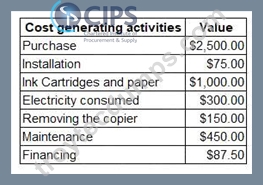

When devising a business case for purchasing a new copier, Maria analyses its whole-life costs as following:

Though cost generating activities are identified, she has not categorised the costs. What is the total value of copier's end of life costs?

- A. $75

- B. $300

- C. $150

- D. $450

Answer: C

Explanation:

Life cycle costing is a key asset management tool that takes into account the whole of life implications of planning, acquiring, operating, maintaining and disposing of an asset.

The process is an evaluation method that considers all ownership and management costs. These include;

- Concept and definition;

- Design and development;

- Manufacturing and installation;

- Maintenance;

- Support services; and

- Retirement, remediation and disposal costs.

End of life costs often comprise of decommissioning, removing and disposal costs. In the copier scenario, the end of life costs equal to removal cost, which is $150.

NEW QUESTION # 70

Which of the following provides in-depth detail for both functional and non-functional require-ments and covers assumptions, constraints, performance, dimensions, weights and reliability of a product?

- A. Statement of work

- B. Design specification

- C. Performance specification

- D. Tolerance

Answer: B

Explanation:

Design specification is a detailed document providing a list of points regarding a product or pro-cess. For example, the design specification could include required dimensions, environmental fac-tors, ergonomic factors, aesthetic factors, maintenance that will be needed, etc. It may also give specific examples of how the design should be executed, helping others work properly (a guideline for what the person should do).

Performance specification is written requirement that describes the functional performance criteria required for a particular equipment, material, or product.

Tolerance is the permissable limit of a variable used to define a product Statement of work is the document that captures and defines all aspects of a project, including the activities, deliverables and the timetable for the project.

Reference: CIPS study guide page 118

LO 3, AC 3.1

NEW QUESTION # 71

ABC Ltd has recently set up a stationery contract with a large stationery provider, obtaining fixed prices on core stationery items. The brochures have been distributed within ABC Ltd and one of the key users wants to order a corner desk and office chair from the brochure. Is this within scope?

- A. Yes, because the contract is with the company and not just stationery

- B. No, because the corner desk wouldn't match existing furniture

- C. Yes, because the office equipment is in the brochure and must be covered

- D. No, because the contract is for stationery only and not furniture

Answer: A

NEW QUESTION # 72

What is a form of testing used to establish if a supplier is meeting the requirements of a specification?

- A. Performance testing

- B. Functional testing

- C. Acceptance testing

- D. User testing

Answer: C

Explanation:

Detailed Explanation:Acceptance testing verifies that the supplied product meets the buyer's specification before it is formally accepted. This type of testing typically occurs during delivery or installation phases.

Reference: CIPS Level 4, Quality Assurance in Procurement.

NEW QUESTION # 73

When should procurement professional tolerate a risk?

- A. When the risk causes some trivial annoyance

- B. When the risk breaks the relationship with the strategic supplier

- C. When the risk may disrupt the production

- D. When the risk imposes an existential threat

Answer: A

Explanation:

Risk control is the process by which an organization reduces the likelihood of a risk event occurring or mitigates the effects that risk should it occur. Our preferred way to determine your risk control strategy is to use the four T's Process:

Transferring Risk can be achieved through the use of various forms of insurance, or the payment to third parties who are prepared to take the risk on behalf of the organization Tolerating Risk is where no action is taken to mitigate or reduce a risk. This may be because the cost of instituting risk reduction or mitigation activity is not cost-effective or the risks of impact are at so low that they are deemed acceptable to the business (such as some trivial annoyance). Even when these risks are tolerated they should be monitored because future changes may make it no longer tolerable.

Treating Risk is a method of controlling risk through actions that reduce the likelihood of the risk occurring or minimize its impact prior to its occurrence. Also, there are contingent measures that can be developed to reduce the impact of an event once it has occurred.

Terminating Risk is the simplest and most often ignored method of dealing with risk. It is the ap-proach that should be most favored where possible and simply involves risk elimination. This can be done by altering an inherently risky process or practice to remove the risk. The same can be used when reviewing practices and processes in all areas of the business.

If an item presents a risk and can be changed or removed without it materially affecting the busi-ness, then removing the risk should be the first option considered; rather than attempting the treat, tolerate or transfer it.

Reference:

LO 3, AC 3.3

NEW QUESTION # 74

......

L4M2 Premium Exam Engine - Download Free PDF Questions: https://www.troytecdumps.com/L4M2-troytec-exam-dumps.html

Instant Download L4M2 Free Updated Test Dumps: https://drive.google.com/open?id=1mbcL-OEhuXfRuRFc0jMJTH4oF2Z4StOg