![]()

[UPDATED 2026] IIA-CIA-Part2 dumps Free Test Engine Verified By Certified Experts

Realistic IIA-CIA-Part2 Accurate & Verified Answers As Experienced in the Actual Test!

IIA-CIA-Part2 exam is an essential certification for internal auditors looking to demonstrate their expertise and advance their careers. IIA-CIA-Part2 exam covers a wide range of topics related to internal auditing, and passing it requires a thorough understanding of the internal audit process, risk management, governance, and ethical principles. Candidates must meet the IIA's eligibility requirements and pass the exam with a score of at least 600 out of 800 to earn this certification.

NEW QUESTION # 379

A bakery chain has a statistical model that can be used to predict daily sales at individual stores based on a direct relationship to the cost of ingredients used and an inverse relationship to rainy days. What conditions would an auditor look for as an indicator of employee theft of food from a specific store?

- A. On a sunny day, total sales are less than expected when compared to the cost of ingredients used.

- B. Both total sales and cost of ingredients used are greater than expected.

- C. On a rainy day, total sales are greater than expected when compared to the cost of ingredients used.

- D. Both total sales and cost of ingredients used are less than expected.

Answer: C

Explanation:

In the scenario provided, the bakery chain's statistical model predicts that daily sales should have an inverse relationship with rainy days, meaning that on rainy days, sales are generally expected to be lower. However, if an auditor notices that on a rainy day, total sales are greater than expected when compared to the cost of ingredients used, this could indicate potential employee theft of food. The reasoning is that if sales are unusually high despite weather conditions that typically depress sales, it may be that the reported sales are inflated or that ingredients are being used without corresponding sales being recorded, which could suggest theft.

IIA Reference:

IIA Standard 1220: Due Professional Care implies that auditors should consider the likelihood of significant errors, fraud, or noncompliance when assessing risks and performing audit procedures. Unusual patterns or deviations from expected results, as seen in this scenario, should raise red flags for potential fraudulent activity, such as theft.

NEW QUESTION # 380

An organization's internal auditors are reviewing production costs at a gas-powered electrical generating plant.

They identify a serious problem with the accuracy of carbon dioxide emissions reported to the environmental regulatory agency, due to computer errors. The auditors should immediately report the concern to:

- A. The regulatory agency.

- B. The risk management function.

- C. A plant health and safety officer.

- D. Plant management.

Answer: D

Explanation:

Section: Volume A

NEW QUESTION # 381

When planning an audit engagement, what should an internal auditor first consider when assessing the risk of fraud in the area to be audited?

- A. Management's risk appetite.

- B. Impact of and exposure to fraud.

- C. Organizational structure.

- D. Existence of evidence of fraud.

Answer: B

NEW QUESTION # 382

In a small internal audit function, a single auditor is responsible for conducting the entire audit engagement.

In this situation, what is the benefit of using a checklist as part of an engagement work program?

- A. Allocation of tasks and responsibilities within the team.

- B. Retention of an audit trail regarding completion of tasks.

- C. Facilitation of review by business representatives involved.

- D. Overview of results from previous audits.

Answer: B

Explanation:

According to the CIA study materials, in small audit functions where one person conducts the engagement, a checklist ensures that tasks are documented and provides a record of completion. This creates a reliable audit trail and supports supervisory review (per Standard 2330 - Documenting Information).

* Option A does not apply since only one auditor is involved.

* Option B is incorrect because checklists are not primarily for business representatives.

* Option C is incorrect: prior audit results would be found in past reports, not a checklist.

Therefore, the primary benefit in this scenario is retention of an audit trail (Option D).

NEW QUESTION # 383

Which of the following is an advantage of utilizing an external fraud specialist in a suspected fraud investigation?

- A. Increased access to the organization's employees.

- B. Increased access to the organization's software and proprietary data.

- C. Increased ability to preserve evidence and the chain of command.

- D. Increased ability to scrutinize the organization's key business processes.

Answer: C

Explanation:

Utilizing an external fraud specialist in a suspected fraud investigation offers several advantages, particularly in preserving evidence and maintaining the chain of command. This is crucial for ensuring that the investigation is conducted legally and that any findings can be used in potential legal proceedings.

* Expertise in Evidence Handling:

* External fraud specialists typically have specific expertise in collecting, preserving, and documenting evidence in a manner that maintains its integrity. This includes maintaining a proper chain of custody, which is essential for legal admissibility.

* IIA Practice Guide on Fraud Investigations:

* The IIA suggests that involving specialists can enhance the credibility and effectiveness of an investigation. Specialists are trained to handle sensitive evidence and ensure that it is preserved correctly, reducing the risk of contamination or loss.

* Chain of Command:

* Maintaining a clear and secure chain of command during an investigation is critical. An external specialist is often better equipped to manage this process, ensuring that evidence is not tampered with and that all actions are documented appropriately.

* Option A (Increased access to employees): While an external specialist may interview employees, this is not their primary advantage over internal auditors.

* Option C (Increased ability to scrutinize processes): Specialists are skilled at this, but the key advantage lies in evidence preservation.

* Option D (Increased access to software and data): Access to proprietary data is important, but internal auditors usually have this access as well.

Detailed Explanation:Why Not Other Options?

NEW QUESTION # 384

An internal audit team was conducting an assurance engagement to review segregation of duties in the purchasing function. The internal auditors reviewed a sample of purchase orders from the past two year and discovered that 2 percent were signed by employees who were operating in a designated acting capacity due to employee absence. According to IIA guidance, which of the following attributes of information would most likely assist the auditor in deciding whether to report this finding?

- A. Sufficiency

- B. Usefulness

- C. Relevance

- D. Reliability

Answer: A

Explanation:

When deciding whether to report a finding, the sufficiency of the information is critical. Sufficiency refers to the quantity of information obtained to support audit conclusions and recommendations. In this case, the internal auditors need to ensure that the sample size and the evidence collected are adequate to demonstrate that the issue of employees signing purchase orders in a designated acting capacity due to employee absence is significant enough to report. Ensuring sufficiency helps validate that the finding is well-supported and justifies its inclusion in the audit report.

:

The Institute of Internal Auditors (IIA) - Standards for the Professional Practice of Internal Auditing, Standard

2310 - Identifying Information

NEW QUESTION # 385

Which of the following is true regarding the monitoring of internal audit activities?

- A. The board of directors is responsible for the establishment of monitoring polities

- B. Both large and small audit departments must have written policies on monitoring.

- C. The chief audit executive must develop all monitoring policies related to the activity

- D. The form and content of monitoring policies could vary by industry

Answer: D

Explanation:

The form and content of monitoring policies can indeed vary depending on the industry and the specific requirements of the organization. While all internal audit activities require some level of monitoring to ensure effectiveness and compliance with standards, the specific approach and documentation may differ based on industry norms, regulatory requirements, and organizational size and complexity.

The Institute of Internal Auditors (IIA) Practice Guide: Quality Assurance and Improvement Program IIA Standard 1300 - Quality Assurance and Improvement Program

NEW QUESTION # 386

The internal audit activity plans to assess the effectiveness of management's self-assessment activities regarding the risk management process. Which of the following procedures would be most appropriate to accomplish this objective?

- A. Conduct interviews with line and senior management on current practices.

- B. Research and review relevant industry information concerning key risks.

- C. Review corporate policies and board minutes for examples of risk discussions.

- D. Observe and test control and monitoring procedures and related reporting.

Answer: D

Explanation:

Assessing the effectiveness of management's self-assessment activities in the context of risk management requires a thorough examination of the processes that management uses to monitor and control risks. The most effective way to evaluate these activities is to observe and test the control and monitoring procedures in place.

* IIA Standard 2130 - Control:

* This standard highlights the internal audit activity's responsibility to assess whether the organization's controls are adequate to manage risks. Observing and testing controls directly is the most effective way to determine their operational effectiveness.

* IIA Practice Advisory 2130-1:

* The advisory recommends that internal auditors should focus on the design and effectiveness of control activities. Observing and testing controls ensures that the auditor can verify whether management's self-assessments accurately reflect the risk environment.

* Effectiveness of Risk Management Processes:

* To assess the effectiveness of self-assessment, internal auditors need to ensure that the procedures for identifying, assessing, and monitoring risks are robust. Direct observation and testing provide tangible evidence of how these processes are functioning.

* Option A (Reviewing corporate policies and board minutes): This provides context but does not directly assess the effectiveness of control procedures.

* Option B (Conducting interviews): Interviews can provide insights but are subjective and may not reflect actual control effectiveness.

* Option C (Researching industry information): This helps in understanding risks but does not assess how well the organization manages those risks.

Detailed Explanation:Why Not Other Options?Conclusion: Option D is correct as it involves the direct evaluation of the effectiveness of control and monitoring procedures, aligning with IIA's guidance on assessing risk management processes.

NEW QUESTION # 387

During the planning phase of an assurance engagement, the internal audit engagement team identifies and evaluates the inherent fraud risks within the procurement function. What should be the engagement team's next step?

- A. Detect fraudulent activities in the activity under review for the audited period

- B. Evaluate and respond to residual fraud risks that need to be mitigated

- C. Select the appetite level for each inherent fraud risk

- D. Identify and map existing controls to their relevant inherent fraud risks

Answer: D

Explanation:

The risk assessment process in planning begins with identifying inherent risks (risks without considering controls). The next logical step is to identify and map existing controls to those inherent risks to determine whether they mitigate them effectively. Only after this step can residual risk be assessed. Detecting actual fraud (Option B) is not part of planning. Risk appetite (C) is a management responsibility, not audit's. Option D occurs later after evaluating controls.

NEW QUESTION # 388

The audit engagement objective is to identify vendors who might be involved in money laundering processes or tax evasion schemes. How would the internal auditor use data analytics to fulfill this objective?

- A. Run reports listing all credit limit overrides

- B. Run reports listing all instances of delayed revenue recognition

- C. Run reports listing all payments made in countries other than vendor locations

- D. Run three-way match reports, matching invoices, purchase orders, and receiving reports

Answer: C

Explanation:

Comprehensive and Detailed Explanation:

One red flag for money laundering and tax evasion is when payments are routed to locations that differ from vendor headquarters or registration. Running reports on payments made to countries outside vendor locations (A) can highlight potentially suspicious transactions.

* Credit overrides (B) relate to credit risk, not money laundering.

* Delayed revenue recognition (C) relates to earnings manipulation.

* Three-way matches (D) test procurement accuracy but not fraud schemes of this type.

Therefore, the most relevant analytic technique is Option A, which directly targets anomalies that suggest offshore routing, shell companies, or tax avoidance schemes.

NEW QUESTION # 389

According to IIA guidance, which of the following are benefits to the internal audit activity when conducting an assurance mapping exercise?

- A. Identification of gaps in risk coverage, and consolidation of risk reporting efforts.

- B. Resolution of identified testing errors, and minimization of duplicate assurance efforts.

- C. Identification of gaps in risk coverage, and minimization of duplicate assurance efforts.

- D. Resolution of identified testing errors, and consolidation of risk reporting efforts.

Answer: C

NEW QUESTION # 390

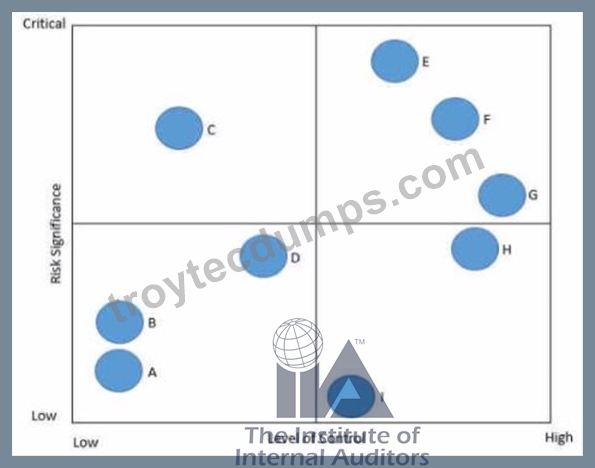

In the following risk control map risks have been categorized based on the level of significance and the associated level of control. Which of the following statements is true regarding Risk C?

- A. The level of control is excessive given the level of risk

- B. The level of control is appropriate given the level of risk

- C. The level of control is inadequate given the level of risk

- D. There is not enough of information to determine whether the controls are appropriate or not

Answer: C

Explanation:

In the risk control map, Risk C is positioned in the upper left quadrant, indicating it is critical (high risk significance) but with a low level of control. This suggests that the current controls are insufficient to mitigate the high level of risk associated with Risk C. For critical risks, a higher level of control is necessary to ensure that the risk is properly managed and mitigated. Reference:

"Internal Auditing: Assurance & Advisory Services" (The Institute of Internal Auditors)

"Risk Management Framework" (COSO)

NEW QUESTION # 391

After becoming aware of control weaknesses indicating that a fraud could have been committed, which of the following actions should an internal auditor take next?

- A. Recommend that a fraud investigation be conducted involving internal auditors, lawyers, investigators, security personnel, and other specialists, as appropriate.

- B. Issue a written report identifying the control weaknesses.

- C. Perform tests directed toward the identification of other fraud indicators.

- D. Notify external auditors of the suspicion that fraud has been committed.

Answer: C

NEW QUESTION # 392

The most effective method of reporting engagement results to management and stimulating action is to:

- A. Deliver a lecture on the engagement results.

- B. Limit verbal commentary and present a series of slides that graphically depict the engagement results.

- C. Use slides to support a discussion of major points.

- D. Distribute copies of the report, ask the participants to read the report, and ask for questions.

Answer: C

NEW QUESTION # 393

The internal audit activity has adopted the balanced scorecard approach to assess its performance According to MA guidance which of the following is a key performance indicator relevant to the audit client?

- A. Percentage of planned audits completed

- B. Staff experience

- C. Conformance with the International Professional Practices Framework

- D. Percentage of recommendations implemented by corrective action date

Answer: A

NEW QUESTION # 394

Which of the following conditions are necessary for successful change management?

1. Decisions and necessary actions are taken promptly.

2. The traditions of the organization are respected.

3. Changes result in improvement or reform.

4. Internal and external communications are controlled.

- A. 2 and 3

- B. 2 and 4

- C. 1 and 2

- D. 1 and 3

Answer: D

Explanation:

Successful change management requires prompt decision-making and actions, as well as ensuring that changes lead to improvement or reform. Respecting the traditions of the organization and controlling internal and external communications are important, but not as critical to the success of change management as the necessity for timely actions and positive outcomes. References:

* IIA Practice Guide - Change Management: Facilitating Organizational Change

* IIA Standards - 2210: Engagement Objectives

NEW QUESTION # 395

According to IIA guidance which of the following statements is true regarding the annual audit plan?

- A. The CAE may make adjustments to the annual audit plan as needed without senior management or board approval.

- B. The chief audit executive (CAE) may incorporate risk information, including risk appetite levels from management for the audit plan at her discretion.

- C. The annual audit plan should only be adjusted in response to problems with resourcing, scope, and data availability.

- D. In an immature risk management environment it is preferable for the CAE to rely solely on her judgment regarding risk identification and assessment to develop the audit plan.

Answer: B

Explanation:

According to the Institute of Internal Auditors (IIA) guidance, the chief audit executive (CAE) should develop a risk-based audit plan that takes into account the organization's risk management framework, including its risk appetite levels. This aligns with Standard 2010 - Planning, which states that the CAE must establish a risk-based plan to determine the priorities of the internal audit activity, consistent with the organization's goals. Risk appetite levels from management are a critical component of understanding the organization's risk profile and should be incorporated into the audit plan. Thus, the CAE may incorporate risk information, including risk appetite levels from management, at her discretion.

Reference: IIA's International Standards for the Professional Practice of Internal Auditing, Standard 2010 - Planning.

NEW QUESTION # 396

A chief audit executive's report to the board showed a significant trend of recent aud4s going over planned budgeted hours. Which of the following factors could cause this trend?

- A. Poor engagement supervision

- B. ineffective board reporting

- C. Limited staff resources

- D. Untimely observation follows up and closure

Answer: A

NEW QUESTION # 397

A governmental auditor was assigned to determine reasons why the students in one region scored significantly higher on education evaluation tests than did the students in another region. Previous research showed that there is a direct correlation between public financial support and student results. Which of the following is most likely to explain the difference in the regional results?

- A. The more successful region has increased educational spending by an average of 10 percent each year for the last three years, whereas the other region's increase averaged only three percent.

- B. A higher percentage of the general tax fund is spent on education in the more successful region than in the other region.

- C. The more successful region spends 30 percent more money on education than does the other region.

- D. The more successful region spends more money per student on education than does the other region.

Answer: D

Explanation:

Section: Volume A

NEW QUESTION # 398

What is the primary purpose of issuing a preliminary communication to management of the area under review?

- A. To help management develop more responsive and timely action plans

- B. To formally report medium- and high-risk observations in writing

- C. To improve the internal audit key performance indicators

- D. To build good relations with management

Answer: A

Explanation:

The primary purpose of issuing a preliminary communication to management of the area under review is to help them develop more responsive and timely action plans. Preliminary communications, such as interim reports or discussions, inform management about the audit's progress, preliminary findings, and potential issues. This early communication allows management to begin addressing identified issues before the final report, leading to more timely and effective corrective actions. It also fosters collaboration and ensures management is engaged in the remediation process from the outset.References: The IIA's International Standards for the Professional Practice of Internal Auditing, Standard 2410.A1 - Communication Criteria.

NEW QUESTION # 399

New credit policies have been implemented in an automated order-entry system to improve the collection of receivables. Sales management has compiled several examples that show decreased sales and delayed order entry, and contends that these examples are a direct result of the new credit-policy constraints. Sales management's data and information provide.

- A. Irrelevant and argumentative information.

- B. A statistically valid conclusion about the impact of the new credit policies on customer goodwill.

- C. Evidence that the new credit policies do not meet the stated corporate objective to improve collections.

- D. Feedback control data.

Answer: D

Explanation:

Section: Volume A

NEW QUESTION # 400

According to IIA guidance, which of the following is true regarding audit supervision?

1.Supervision should be performed throughout the planning, examination, evaluation, communication, and follow-up stages of the audit engagement.

2.Supervision should extend to training, time reporting, and expense control, as well as administrative matters.

3.Supervision should include review of engagement workpapers, with documented evidence of the review.

- A. 1 and 2 only

- B. 1 and 3 only

- C. 1, 2, and 3

- D. 2 and 3 only

Answer: C

NEW QUESTION # 401

Insurance companies often receive electronic hospitalization claims directly from hospitals. Which of the following control procedures would be most effective in detecting fraud in such an environment?

- A. Develop batch controls over all items received from a particular hospital and process those claims in batches.

- B. Use generalized audit software to match the claimant identification number with a master list of valid policyholders.

- C. Use integrated test facilities to test the accuracy of processing in a manner that is transparent to data processing.

- D. Develop monitoring programs to identify unusual types of claims or an unusual number of claims by demographic class for investigation by the claims department.

Answer: D

Explanation:

Section: Volume A

NEW QUESTION # 402

An audit identified a number of weaknesses in the configuration of a critical client/server system. Although some of the weaknesses were corrected prior to the issuance of the audit report, correction of the rest will require between 6 and 18 months for completion. Consequently, management has developed a detailed action plan, with anticipated completion dates, for addressing the weaknesses. What is the most appropriate course of action for the chief audit executive to take?

- A. Reassign information systems auditors to assist in implementing management's action plan.

- B. Evaluate the ability of the action plan to correct the weaknesses and monitor key dates and deliverables.

- C. Assess the status of corrective action during a follow-up audit engagement after the action plan has been completed.

- D. Assess the effectiveness of corrections by reviewing statistics related to unplanned system outages, and denials of service.

Answer: B

Explanation:

Section: Volume E

NEW QUESTION # 403

......

Latest IIA IIA-CIA-Part2 Practice Test Questions: https://www.troytecdumps.com/IIA-CIA-Part2-troytec-exam-dumps.html

May-2026 Pass IIA IIA-CIA-Part2 Exam in First Attempt Easily: https://drive.google.com/open?id=1n8BIgp8SYonM3bkF168qNeCJekPO_xj2